What is an RRSP?

An RRSP is a Registered Retirement Savings Plan. It is a registered account into which you and your spouse or partner can contribute money for your retirement.

RRSP contributions can be used to reduce the amount of tax you pay. And any income you earn in the RRSP is (usually) exempt from tax while it remains in the plan.

We refer to them as a vehicle for savings as they help you save on two separate fronts:

- You are setting aside money for your retirement; and

- You are saving money in terms of minimizing your tax obligations.

Benefits to RRSPs

RRSPs come with three major benefits:

Tax Deductible Contributions

Any contributions you make to your RRSP, within the prescribed limits, are tax deductible. Additionally, the income from the RRSP is tax-sheltered. So, you can use your RRSP as a tool to minimize your tax obligations.

Tax Deferred

You pay tax on the financial gains from your RRSP when you retire. Since your income is likely to be significantly lower when you retire, you’ll likely be in a lower tax bracket. Meaning you pay less tax tomorrow on the income you earn today.

Security in Retirement

By taking advantage of the tools the Canadian Government provides for retirement planning, you can feel secure in your future.

Types of RRSP:

Deposit-Type RRSP

These are the RRSPs available through your financial institution.

Your key choices with these accounts include:

- Term of the deposit;

- Frequency of interest calculations; and

- Frequency of payment to the RRSP.

RRSP Mutual Funds

Mutual funds can be held in an RRSP. Income and capital gains from these are usually used to purchase additional units in the funds.

These funds often invest in stocks, money markets, and securities.

Self-Directed RRSP

These plans are best suited to those with considerable investment experience and time to manage the fund, since the time investment can be substantial.

Spousal or Common-Law Partner RRSPs

Spouses can help build their partner’s retirement savings by contributing to their RRSP.

Withdrawing Money from Your RRSP

Generally speaking, you can withdraw money from your RRSP. But it isn’t advisable unless it’s for purchases supported by RRSPs.

Some RRSPs, like locked-in RRSPs, don’t allow you to make withdrawals for a certain period.

Withdrawals before retirement are immediately subject to withholding tax. The amount of tax payable varies depending on the amount withdrawn. The upper limit is for withdrawals in excess of $15,000, which are subject to a withholding tax rate of 30%.

RRSPs aren’t the best vehicle to save for goals other than retirement and those exceptions outlined below:

First Home Buyers

Home buyers can withdraw up to $35,000 for the down payment on their first home, tax-free.

This withdrawal comes with the caveat that the money must be repaid to the RRSP within 15 years. This repayment period starts the second year after you first withdrew the funds. So, if you withdraw funds this year (in 2019), your repayment period will commence in 2021.

You can find out more about the repayment period on the website for the Canadian Government.

Lifelong Learning

Canadian residents who intend to commence full-time studies are eligible to withdraw up to $10,000 from their RRSP in a calendar year to support their studies. Though, you are limited to $20,000 in withdrawals from your RRSP for your education.

Again, the withdrawals must be repaid within 10 years.

You can read more about withdrawals for lifelong learning here.

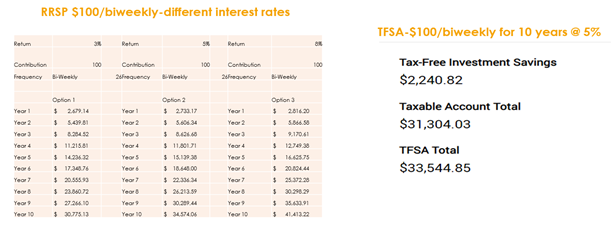

RRSPs VS TFSAs

Tax Free Savings Accounts (TFSAs) allow your investment to grow tax free, but don’t offer the same tax deductions that RRSPs do. TFSAs are useful tools for your immediate financial goals, but can also be used as a vehicle for retirement savings in some situations.

How Much Money Do I Need to Retire?

This is where retirement planning gets tricky. How much money you need to retire depends largely on your assets, your plans, your lifestyle, and what income you’d like to draw from your RRSP annually.

To determine how much money you’ll need to retire, it’s best to talk to a financial planner or advisor.

Budgeting will become crucial during your retirement. You can read more about retirement budgeting in our article on the topic.

The Road to Retirement Planning

Osoyoos Credit Union has been helping its members save for retirement since 1946. We understand the complexities of the road to retirement planning and that each person walks a different path on their way.

For assistance, you can use our RRSP Calculator Tool. Or check out our Retirement Savings FAQs.

Otherwise, if you’d like to receive advice and a plan tailored to your situation, Contact an OCU Advisor to plan your road to retirement.